12 min de lectura

12 min de lectura

After reducing its reliance on Russian energy supplies, the EU has found itself facing a choice that goes far beyond energy policy. The southern vector, above all the Maghreb, is increasingly seen as part of Europe’s new energy architecture: Algeria can quickly add volumes of pipeline gas, while Morocco is positioning itself as a platform for the “green” transformation and future energy value chains. Yet the key bet here is not only about supply, but about political impact: an energy partnership can become a bridge toward building a “belt of stability” in the EU’s Southern Neighbourhood — one on which Europe depends no less than on its Eastern neighbourhood.

However, without a political framework and targeted investment, energy cooperation risks remaining a situational deal rather than the foundation of stable relations. The absence of interconnectors, governance challenges in the sector, the question of Western Sahara, and Algerian–Moroccan rivalry all directly shape whether the EU can turn the southern vector from a mere “resource market” into a space of partnership and stability.

The southern vector in European energy policy is often described as the “closest” and therefore seemingly natural anchor for diversification, especially after the reduction of imports from Russia and within the logic of REPowerEU. The Maghreb does indeed appear attractive: geographic proximity, existing supply routes to the EU’s southern member states, historically dense ties, and significant investment potential that can be “packaged” not only as energy deals but as a broader development partnership. According to the European Commission's REPowerEU progress review, Algeria remains a major and reliable gas supplier to the EU, underscoring the continued importance of the southern vector.

Yet this is precisely where the key trap emerges: the success of the southern vector is determined not only by how much gas or how many megawatts Algeria or Morocco can offer, but by whether the EU can turn energy into a manageable, predictable, and scalable instrument of foreign policy — in other words, a bridge to stability rather than a stop‑gap tool for “plugging shortages.”

First, even with a resource base and willingness to supply additional volumes, Europe faces internal infrastructural constraints. The clearest example is the insufficient capacity of interconnectors between Spain and France. The Iberian Peninsula has long functioned as an energy island – a structural bottleneck the EU is now addressing with a EUR 1.6 billion EIB investment in the Bay of Biscay interconnector, set to raise exchange capacity from 2.8 GW to 5 GW. As a result, the southern vector often functions as a solution for individual member states, but does not automatically become a systemic safeguard for the Union as a whole. This means that any discussion of the Maghreb as a pillar of Europe’s new energy architecture inevitably runs into the logic of the EU’s own network: diversifying suppliers without diversifying and strengthening internal “arteries” does not yield a full strategic payoff.

Second, the southern vector cannot be considered outside the region’s political economy. Unlike the technocratic notion of a “market of suppliers,” the Maghreb is a space where energy infrastructure and routes can become part of political competition and diplomatic conflict. Algerian–Moroccan rivalry, the issue of Western Sahara, and mutual suspicions turn even promising projects into fragile arrangements: they depend not only on price or technology, but on political temperature, the security environment, the domestic legitimacy of decisions, and regional balances. For the EU, this creates a practical challenge: building a “belt of stability” through energy is possible only when energy arrangements are reinforced by a broader framework of presence — investment, institutional, and security — and when the risks of conflict are not merely acknowledged, but actively managed.

Third, European energy policy is shaped simultaneously by two time horizons that are not always easy to reconcile. In the short term, the EU needs reliable non‑Russian volumes and relatively fast solutions to stabilize the energy market. In the long term, the logic of decarbonization prevails: the Green Deal, climate‑neutrality targets, and industrial transformation. In the Maghreb context, this means that the “gas” and “green” parts of the agenda should not be set against each other. If the EU invests only in fossil‑fuel infrastructure without a plan for compatibility with future low‑carbon value chains, it risks creating new dependencies and stranded assets. If, on the other hand, it bets only on green technologies, the impact may be too slow for current needs. That is why the quality of investments and the design of partnerships become decisive: solutions must simultaneously strengthen energy resilience “here and now” while preserving room for technological conversion and a transition “later.”

Ultimately, the southern energy vector is, for the EU, a test of its ability to combine internal infrastructure policy, an external investment presence, and neighborhood policy into a single strategic construct. This is precisely why energy can become a bridge toward stable contacts and a “belt of stability” in the Southern Neighbourhood — but only if the EU treats the Maghreb not as a temporary substitute for supplies, but as a space for long‑term partnership, where stability and mutual benefit require systemic investment and a political framework.

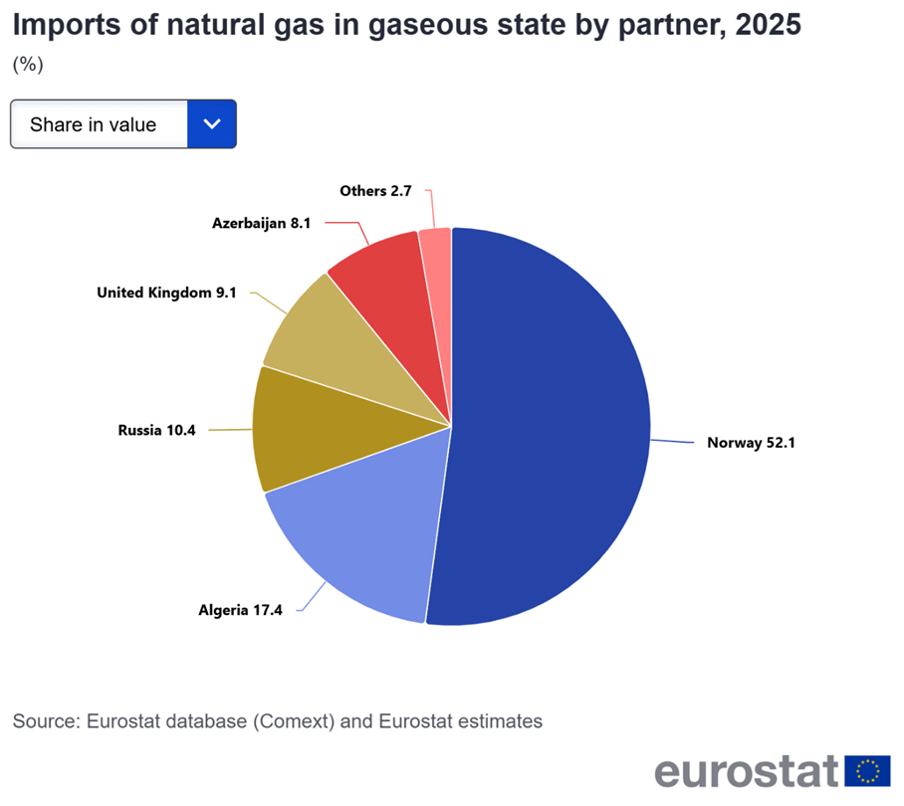

In the EU’s southern energy equation, Algeria looks like the most obvious partner because it offers what Europe lacks in a period of turbulence: relative geographic proximity, existing pipeline routes, and the ability to support the energy system without constant exposure to global competition for LNG tankers and maritime chokepoints. This is why, after 2022, the Algerian track began to be perceived not merely as one option among others, but as a practical instrument for rapidly strengthening resilience, especially for the EU’s southern member states. Italy and Algeria, for instance, agreed to increase gas supply to 9 bcm/year by 2024 via the TRANSMED pipeline. In this sense, Algeria is the short distance: it can deliver an effect faster than any major green projects that require years of preparation, financing, and infrastructure roll-out.

However, a strategic partnership with Algeria cannot be reduced to the logic of “more cubic meters equals more security.” Reality is more complex, and it is precisely in that complexity that the EU’s key lessons lie. First, even when Algeria has the potential to increase supplies, the impact on the overall European energy situation remains uneven: gas enters Europe through specific routes and primarily strengthens those markets that are physically closer or better connected. Without stronger internal EU interconnectors, Algeria does not become a “supplier for everyone”; it remains critically important, but mainly for part of the Union.

Second, Algeria’s energy sector has its own “internal limits”: aging infrastructure, regulatory constraints, and a nationalistic investment environment that deters foreign capital — all of which directly affect whether the country can sustainably scale exports. Italy, Algeria's largest EU customer, already saw Algeria's share of its gas imports fall from 44% in 2022 to 36% in 2024. The impact on the overall European energy situation remains uneven: gas enters Europe through specific routes and primarily strengthens those markets that are physically closer or better connected.

There is also the factor of time horizon: the EU thinks in terms of transition, decarbonization, and a future hydrogen economy, whereas Algeria's revenue model remains largely tied to hydrocarbons. The most recent EU-Algeria High Level Energy Dialogue (February 2026) reflected this tension, with discussions covering gas cooperation, renewables, and hydrogen, signaling that Brussels is pushing to broaden the relationship beyond fossil fuels. This creates not a conflict but a tension of interests that must be calibrated correctly so that the partnership does not turn into a temporary transaction.

Therefore, for the EU, Algeria is both an opportunity and a challenge. The opportunity is that it can help cushion Europe during the transition period. The challenge is that achieving a real strategic payoff requires a different quality of engagement: not only buying a resource, but building a framework of trust and predictability that includes investment in sector modernization, infrastructure, transparent rules of the game, and the gradual alignment of the energy dialogue with the EU’s long‑term objectives.

In the logic of a “belt of stability,” this is especially important: stable supplies emerge where there are stable institutional and economic conditions — not only where there are deposits.

If Algeria in this story is a partner for “today’s” energy security, then Morocco is more of a partner for “tomorrow’s” architecture. The country does not possess comparable reserves of gas or oil; instead, it is building its energy role around renewable generation and the idea of turning geographic proximity to Europe into an economic advantage. The EU-Morocco Green Partnership, signed in October 2022 and the first such agreement under the external arm of the European Green Deal, established a policy dialogue on climate, energy, and the green economy, explicitly including the development of the hydrogen economy. For the EU, this opens up a different type of engagement: not rapid supply substitution, but an investment partnership capable of creating new value chains.

Morocco's ambitions in this space are substantial. In March 2024, the government launched the Morocco Offer investment program, allocating 300,000 hectares for renewable energy and green hydrogen projects worth approximately $32.5 billion, focused on green ammonia, e-fuels, and green steel. By March 2025, five investor consortia had been pre-selected for the first phase. The country aims to increase renewables' share to 52% of total installed capacity by 2030. Germany, the Netherlands, and other European partners have already signed bilateral action plans and MoUs supporting hydrogen, port infrastructure, and green shipping corridors.

This is precisely where energy works best as a “bridge.” The Moroccan track allows the EU to connect its energy interests with the broader logic of the European Neighbourhood Policy: development, infrastructure, technological cooperation, employment, and strengthening partners’ resilience. In a broader perspective, this fits into the European idea of stability through development, where a partner does not merely supply a resource but becomes a participant in a shared transformation. It is worth noting, however, that starting from 2026, electricity will fall under the EU's Carbon Border Adjustment Mechanism (CBAM), which shifts bargaining power toward Brussels and reinforces the urgency of decarbonization for Moroccan producers.

However, Morocco’s potential does not exist in a vacuum. It runs up against political risks and regional tensions (particularly around Western Sahara) as well as the need for large, long-term investments that require a high level of predictability and trust.

This is important to emphasize to avoid creating illusions: the “green” agenda in the South can become a success story for the EU, but it is neither automatic nor a quick fix. That is why Morocco should be presented here not as an alternative to Algeria, but as another layer of the same strategy: Algeria can strengthen resilience in the short term, while Morocco can help Europe invest in a future energy model and, more broadly, in the long-term stability of the Southern Neighbourhood.

At the moment when the EU is trying to build a long-term “belt of stability” in North Africa, the most difficult element of this construction is not a lack of resources or even a shortage of money, but the region's political geometry. Since 2021, when Algeria severed diplomatic ties with Morocco, the two neighbors have been embroiled in a deep crisis. According to the International Crisis Group, incidents in Western Sahara risk bringing the two countries to blows, and mutual suspicions have hardened significantly.

Algeria and Morocco often appear to Brussels as two separate tracks of cooperation — each important, each promising, each with its own set of interests and formats for dialogue with the EU. In practice, however, these tracks intersect: rivalry between the two countries means that energy here almost never remains “pure economics.” It quickly becomes a language of political signaling, an instrument of competition for influence, and a lever of pressure. Both countries have taken to using energy and trade as tools for furthering their strategic ambitions — Algeria through its gas leverage over Italy and Germany, Morocco through the Nigeria pipeline project, and Gulf partnerships. That is why any European strategy that ignores this background risks working only for as long as the region retains a kind of “fair weather.”

The central knot of the rivalry is the Western Sahara issue and Algeria’s associated support for the Polisario Front. The most vivid energy manifestation of this conflict was Algeria's 2021 decision to halt gas exports via the Maghreb-Europe pipeline through Moroccan territory. As one recent analysis by the German Marshall Fund notes, Algeria's rivalry with Morocco directly shapes its energy diplomacy and constrains the EU's ability to treat the northern corridor as a coherent supply zone, with the geopolitical complexity deepening further given Algeria's arms dependency on Moscow.

For Morocco, this is a matter of territorial integrity and domestic legitimacy — hence a red line that shapes the overall logic of its foreign policy. For Algeria, support for Polisario is not only an element of regional politics, but also a way to preserve its own role in the balance of power in the Maghreb. As a result, a conflict that at first glance may seem “separate” from energy becomes woven into energy routes, the prospects for major infrastructure projects, and the overall level of trust. And this is where the EU must understand: even the best technical projects can lose their meaning if they do not fit the region’s political reality.

This is precisely why EU energy cooperation with the Maghreb is vulnerable to sharp fluctuations. A deterioration in diplomatic relations or an escalation in rhetoric can be enough for supply, transit, or coordination to come under pressure. For Europe, this means that a bet on the southern vector cannot be built exclusively on bilateral “deals with each other.” If the EU wants energy to serve as a bridge to stable contacts, it needs at least minimal mechanisms that reduce the risk of a “domino effect,” in which tensions between Algeria and Morocco destabilize the broader regional picture.

Here, a cautious parallel with the Eastern Neighbourhood is appropriate: both in the East and in the South, the EU faces the reality that major political conflicts can reshape energy and infrastructure decisions. The difference is that in the Maghreb, Europe still has more room for a “positive agenda” — investment, development, technological cooperation, long-term infrastructure projects — and it is precisely this space that can be used as a safeguard. But the underlying logic is the same: if the EU does not incorporate political risks into the design of its energy partnerships, it condemns itself to reactive crisis management, where every escalation will require “firefighting” rather than steady movement toward long-term resilience.

Building a belt of stability through energy is possible, but only if Europe understands that the stability of routes and the stability of the region are interconnected, and that investment without a political framework can sometimes only increase the cost of future crises.

When the EU speaks about North Africa as part of a new European energy architecture, the key question is not “whether to cooperate,” but “how” — with what logic, which instruments, and on what time horizon. In practice, the Union has at least three distinct trajectories, each responding differently to the dilemma between rapid energy insurance and the long-term ambition to turn energy into a bridge to stability in the Southern Neighbourhood.

The simplest option is to continue with parallel bilateral tracks: deepening cooperation with Algeria and Morocco separately, without moving into more complex formats in which the EU would have to act as a moderator or mediator between two competitors. This model is attractive for its political “lightness”: it allows the EU to avoid topics that quickly become toxic and to concentrate on practical matters — contracts, investment agreements, and targeted projects. Yet its limitation is obvious: a bilateral approach does not remove regional fragility; it merely teaches the EU to live with it. It may work in periods of relative calm, but when rivalry intensifies or trust erodes, energy once again comes under risk, and Europe effectively pays for the absence of systemic safeguards.

The second option — and the one that best fits the idea of a “belt of stability” — is to treat infrastructure and investment as a form of strategy rather than a collection of individual projects. In this approach, the EU recognizes that diversification works only when Europe’s internal network can distribute the resource, and when partner countries have the institutional and regulatory capacity to be predictable suppliers or production platforms.

That means investing not only “there,” in the Maghreb, but also “here,” at the heart of Europe: in connections, system flexibility, interconnectors, and network modernization. In parallel, it means investing in partners’ energy sectors in ways that strengthen not only supply volumes or generated megawatts, but broader resilience: governance, transparent rules of the game, infrastructure development, and socio-economic effects. This is how energy can function as a bridge: it gives the EU a concrete foundation for a longer-term partnership in which stability is built through development and interdependence, not only through crisis-era purchases.

The third option is a green technological bet, with the EU focusing primarily on cooperation with Morocco as a future platform for renewable energy, green hydrogen, and derivative products. This approach aligns best with the EU’s climate logic and can create deeper integration into future value chains. But it has two natural constraints: time and cost. Green projects rarely deliver a quick impact; they require long investment cycles, infrastructure, regulatory frameworks, and, crucially, a stable political environment. Therefore, a “green bet” can be a strong element of the long game, but it cannot fully replace short-term solutions where the EU seeks to rapidly strengthen energy resilience.

In practical terms, these three packages are not necessarily mutually exclusive, the EU can combine them, but it is important not to lose the strategic backbone. If the goal is not only physical diversification of supplies, but the creation of a southern belt of stability, then energy must become an “organizing principle” of a broader partnership: grounded in a clear understanding of Europe’s own infrastructural constraints, the Maghreb’s regional political risks, and the long arc of the green transition. This linkage —resources, investment, institutions, and stability — is what can turn the southern vector into a long-term anchor rather than a situational response to the next crisis.

The views, thoughts, and opinions expressed in the papers published on this site belong solely to the authors and not necessarily to the Transatlantic Dialogue Center, its committees, or its affiliated organizations. The papers are intended to stimulate dialogue and discussion and do not represent official policy positions of the Transatlantic Dialogue Center or any other organizations with which the authors may be associated.