10 min read

10 min read

In recent years, competition over energy resources has taken on a new form: energy is increasingly treated not only as a commodity, but also as an instrument of political influence. Russia’s full-scale war against Ukraine has been a key catalyst for this shift in Europe. It exposed how vulnerable the EU can be when a single supplier dominates its energy balance, and it accelerated European efforts to diversify gas and oil supply routes.

The destruction of the Nord Stream pipeline system further reinforced this shift, forcing European policymakers to rethink not only supply sources but also the resilience of energy infrastructure.

In this context, the European Union launched a policy of phasing out Russian energy imports under the REPowerEU framework. Yet the core change is not merely substituting one supplier for another. The more consequential shift is the transformation of dependency itself: as Russian volumes decline, the strategic weight of transit nodes, infrastructure bottlenecks, and market access rules grows.

This is where the Southern Gas Corridor becomes politically significant, and where Türkiye aims to translate geography and infrastructure into long-term leverage. Resource-related dynamics beyond Europe, including competition over oil and over critical minerals, reinforce the same broader point: control over access and transport routes increasingly shapes foreign policy choices.

This article argues that Türkiye’s rising role in Europe’s gas architecture does not automatically mean a one-to-one replacement of dependencies, but it does create a new matrix of interdependence that affects the EU’s bargaining position, Russia’s options, and the strategic calculations of regional suppliers. Managing these risks will require clearer-eyed policy choices from European decision-makers.

After 2022, the EU’s gas strategy shifted from treating diversification as a long-term objective to treating it as a near-term security task. This did not mean that Europe could “swap out” Russian gas overnight. Instead, it pushed the EU to do several things at once: reduce consumption, expand LNG capacity, strengthen interconnectors, and increase pipeline imports from alternative partners.

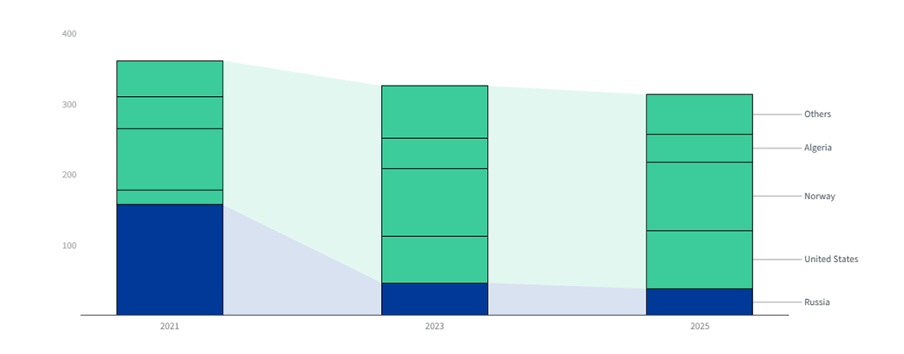

That shift is visible in the numbers. Russia’s share of EU pipeline gas imports fell from over 40% in 2021 to about 11% in 2024. In 2024, the EU’s largest gas suppliers were Norway (91.1 billion cubic meters, bcm) and the United States (45.1 bcm), followed by Algeria (39.2 bcm), while Azerbaijan supplied 11.7 bcm (a smaller share, but still material in diversification terms). The rapid growth of LNG imports, particularly from the United States, has therefore become one of the central pillars of Europe’s post-2022 diversification strategy. Politically, the EU formalized this direction under REPowerEU, which sets out a gradual phase-out of Russian energy imports.

In that context, the Southern Gas Corridor (SGC) is best understood not as a single “replacement route,” but as one component of a broader diversification mix. It is a chain of pipelines that brings Caspian gas westward through the South Caucasus and Türkiye into EU markets via Greece and the Adriatic route to Italy. In simple terms, it is built from three main links:

The corridor’s long-term relevance also depends on production growth in Azerbaijan, which remains the primary upstream supplier through the Shah Deniz field operated by SOCAR and international partners.

This infrastructure matters strategically even if its volumes remain limited compared to what Russia once delivered to the EU. The corridor’s value is not only “how much gas it brings,” but also what kind of option it creates. And what it does create is a functioning southern entry route that can reduce the leverage of any single dominant supplier, especially for parts of Southern and South-Eastern Europe where route alternatives are more constrained.

At the same time, it is important not to overstate what SGC can do. Its impact depends on upstream resource availability, expansion decisions (especially around TANAP/TAP), and Europe’s longer-term trajectory of gas demand under decarbonization policies. This is why the corridor is more plausibly seen as a stabilizing diversification layer rather than a standalone substitute for Russian imports.

In energy debates, Türkiye is often described as a “transit country”, but Ankara’s declared ambition is broader: to become a gas hub. The distinction matters. A transit state mainly earns fees for moving gas across its territory under relatively fixed arrangements. At the same time, Türkiye already hosts one of the remaining Russian export routes to Europe through the TurkStream pipeline, which continues to deliver gas to South-Eastern European markets. A hub, by contrast, aims to become a place where gas can be traded, stored, redirected, and priced with more flexibility, and where market design can shape regional flows.

The “hub status” in Türkiye is not simply a technocratic energy policy goal. It is deeply embedded in the country’s strategic and political self-perception. In official language, energy is framed as part of Türkiye’s role as a central or pivotal state between regions, and as a tool for strengthening strategic autonomy. This framing appears consistently in government narratives about diversifying routes and resources, contributing to regional energy security, and positioning Türkiye as a trade center in energy.

This matters because it means Türkiye’s hub ambition is tied to foreign-policy posture, not only infrastructure. Control over energy routes is treated as a way to reinforce Türkiye’s relevance in relations with the EU, Russia, and Middle Eastern partners, and as a channel to expand diplomatic space even when other political tracks are strained.

Türkiye’s potential influence is unlikely to look like blunt energy coercion. That would be economically costly for Ankara and politically risky given its dependence on European trade and investment. Instead, if the hub vision advances, leverage would more plausibly emerge through calibrated, structural mechanisms, such as:

At the same time, hub status is not achieved through geography alone. It requires credible market rules, sufficient liquidity and storage, and predictability for companies that would rely on Türkiye as a commercial platform. Without those elements, Türkiye risks remaining an important corridor but not a true market-maker.

For the EU, this is not a binary choice between “Russia” and “Türkiye.” But it does highlight a strategic issue: as Europe reduces dependence on a dominant supplier, exposure can shift toward transit and hub nodes. That is a different type of risk. It can be managed, but it requires deliberate diversification policy design, including maintaining multiple routes (LNG and pipelines), investing in cross-border resilience, and avoiding over-concentration in any single corridor.

Russia is unlikely to be “pushed out” of Europe’s broader gas equation overnight, but a stronger Southern Gas Corridor and a more LNG-heavy market can gradually narrow Moscow’s room for maneuver. As the EU’s import portfolio becomes more diversified, Russia’s ability to leverage supply concentration for political or pricing influence tends to weaken, especially in South-Eastern Europe, where alternative routes gain relevance. At the same time, Russia may seek to preserve its position through competitive pricing, contractual flexibility, and by focusing on markets where alternatives remain structurally limited. Or, more radically, by bribing certain key decision-makers, as we are seeing in some Eastern European countries. The net effect is therefore more likely to be a constraint on Russia’s unilateral leverage rather than a rapid elimination of Russian relevance.

A central pillar of Türkiye’s hub ambition is flexibility, and in gas markets, flexibility is increasingly associated with LNG. Compared to pipelines, LNG can be redirected faster, sourced from a wider pool of exporters, and used to respond to short-term price and supply shocks. This is one reason Ankara has invested heavily in expanding regasification capacity and in building a portfolio that combines pipeline inflows with LNG options.

From Türkiye’s perspective, LNG serves three overlapping functions.

First, it is a supply-security hedge. By expanding LNG access, Türkiye reduces its reliance on a small number of pipeline suppliers and rigid long-term contractual structures. In political terms, this diversification supports Ankara’s broader strategy of maximizing room for maneuver – a theme that runs through official statements about energy security, route diversification, and Türkiye’s goal of becoming a regional energy trade center.

Second, LNG is a hub-enabling instrument. A hub is not only about geography; it is about the ability to balance flows and manage uncertainty. LNG infrastructure helps Türkiye position itself not merely as a corridor for fixed volumes, but as a platform that can (at least at the margin) combine different sources and adjust to changes in demand, seasonal conditions, or disruptions elsewhere.

Third, LNG can strengthen Türkiye’s relevance for South-Eastern Europe, where alternatives may be more constrained than in North-Western Europe and where marginal volumes can matter in crisis situations. In practice, Türkiye’s value proposition here is not that it can “replace” EU supplies, but that it can potentially contribute to regional balancing when markets tighten.

This matters because gas markets remain sensitive to abrupt shocks. Unexpected security escalations, such as military operations that raise uncertainty in the wider Middle East, can amplify concerns about supply reliability and trigger price volatility, even when physical disruptions are limited. In periods like these, the market tends to place a premium on flexibility and optionality. That dynamic does not automatically benefit any single actor, but it makes countries with diversified entry points, regasification capacity, and storage options more strategically relevant than they appear during calm periods.

Even with strong geography and infrastructure, Türkiye’s transition from “corridor” to “hub” is not guaranteed. A hub model requires sustained investment, predictable governance, and enough commercial confidence to attract trading activity. Several constraints could therefore slow or reshape Ankara’s plans.

Hub-building is capital-intensive. Expanding storage, upgrading networks, improving interconnectors, and maintaining LNG capacity all require steady financing. Türkiye’s broader economic headwinds can complicate this in two ways:

This does not mean Türkiye cannot advance its hub agenda. It does mean that the pace and scale of that agenda may depend on whether Ankara can mobilize investment without creating additional macroeconomic strain.

Türkiye’s “flexibility narrative” tends to become more attractive during crises, but crises also increase operational and political risk. Sudden escalations in the wider Middle East, such as U.S. military action against Iran or comparable developments that heighten uncertainty, can tighten markets and drive volatility. In such moments, the market often prices in scarcity risk, even before physical disruptions materialize.

For Europe, this can cut both ways:

For Türkiye, recurring shocks can reinforce the argument for hub relevance, but they can also raise concerns among European buyers about predictability and risk premiums.

If Türkiye wants to be seen as a hub for European consumers rather than merely a transit route, the EU will implicitly (and sometimes explicitly) look for predictability, transparency, and rule-based access.

In other words, the limiting factor is not only physical capacity. It is also whether Türkiye can offer the kind of governance environment that European companies and regulators regard as reliable. If EU stakeholders perceive the market as opaque or overly politicized, they may treat Türkiye’s system as a useful corridor in emergencies, but hesitate to treat it as a long-term commercial platform.

From the EU perspective, diversification away from Russia is not meant to create a new single point of dependence elsewhere. Europe’s approach increasingly resembles a portfolio strategy: LNG, multiple pipeline suppliers, demand reduction, and interconnectors. That approach naturally limits how dominant any one corridor, including the southern route through Türkiye, can become.

This is one reason Türkiye’s hub role is more likely to expand as a regional balancing option (especially for South-Eastern Europe) than as a central replacement pillar for the EU as a whole.

Türkiye’s ambition to become a gas hub should be understood as a political-economic strategy, not only an infrastructure project. As the EU reduces reliance on Russian gas, the strategic center of gravity gradually shifts toward a more complex system where routes, flexibility, and governance matter alongside supply volumes.

Importantly, Türkiye is not starting from zero. In recent years, Ankara has made tangible progress in building hub-adjacent capabilities. These developments do not automatically translate into decisive political leverage over the EU, but they do increase Türkiye’s relevance in Europe’s energy-security calculations, especially during periods of market stress, when flexibility and optionality become more valuable than in normal conditions.

For Europe, this matters in two ways. First, Türkiye’s growing capacity to balance pipeline inflows and LNG options can support diversification and improve resilience, particularly for South-Eastern Europe, where route alternatives are often more constrained. Second, it reinforces a broader reality of the post-2022 energy landscape: Europe may reduce dependence on a single dominant supplier while facing a wider set of challenges related to transit nodes, infrastructure bottlenecks, and non-EU governance frameworks. The likely outcome is not a simple “replacement” of one dependency with another, but a new matrix of interdependence that requires deliberate risk management.

For European policymakers, the key challenge will therefore be to design an energy architecture that remains resilient not only to supplier pressure but also to potential leverage emerging from transit hubs and infrastructure bottlenecks.

The views, thoughts, and opinions expressed in the papers published on this site belong solely to the authors and not necessarily to the Transatlantic Dialogue Center, its committees, or its affiliated organizations. The papers are intended to stimulate dialogue and discussion and do not represent official policy positions of the Transatlantic Dialogue Center or any other organizations with which the authors may be associated.