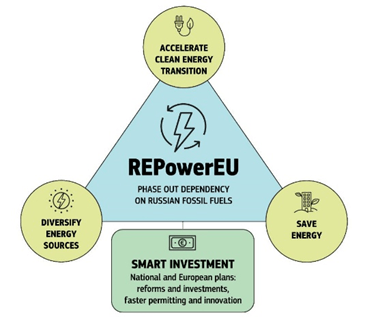

The key to coping with the looming energy crisis is political in nature. This key is the plan, unveiled by the European Commission on May 18 and awaiting approval by the European Council later this June.

If approved, it will give the EU a tangible prospect of ending its reliance on Russian fossil fuels by 2027; if not, it will signal widening gaps among EU members that could be utilized by the Kremlin and the populist forces in Europe.

A more concrete answer to the question “how can Europe survive without Russian energy” comes down to factoring in key variables that will determine EU’s energy outlook:

- curtailing fossil fuels consumption;

- enhancing energy efficiency;

- increasing the share of renewables;

- diversifying external energy resources;

- improving intra-EU infrastructure;

+ temporary measures:

- replacing gas with coal for electricity generation;

- delaying the closure of nuclear power plants.

This strategy of “putting eggs in different baskets” is what might work for the EU. Numbers also suggest that REPowerEU plan targets are deliverable. Reaching a 45% share of renewable energy sources (RES) by 2030 up from the previous one of 40% should not be an Augean task, considering that the EU exceeded its 20% target in 2020 (21.3%).

The trick, however, is in climate neutrality. Under the European Climate Law of 2021, the goal was set to reduce GHG emissions by 55% by 2030. Statistics say that to do it the EU will have to double its current wind annual installation rate. If Russian gas is eliminated as a major transitional energy source, the required pace of installation will probably have to be even higher. In turn, this will require substantial investments. Last year, however, venture capitalists contributed $11.9 billion in RES as against $30.1 billion in blockchain; just 4% of venture capitalists’ money went into energy start-ups. Prompting the investors to “get real” should therefore be the task, since achieving net zero by 2050 requires $3.8 trillion into wind and solar projects as well as $1.5 trillion into green hydrogen (by comparison, REPowerEU provides for just $210 billion for 2022–2027).

Another dimension is replacing Russian gas with other pipeline flows and LNG. At first glance, the outlook is bright: in 2021, Russia exported around 1,670 TWh (155 billion cubic meters) of gas to the EU; meanwhile, the unused capacity for the EU from other pipeline and LNG sources stood at around 1,800 TWh. However, this spare capacity cannot be fully used due to a number of hurdles. This gives the key role to the US. If the current supply of American LNG continues, Europe could receive an additional 63 bcm by the end of the year. But approaching this result will require an energy diplomacy effort to re-route US supplies from other buyers to the EU. Doing the same with another major supplier – Qatar – is not likely due to its long-term contracts with Asian buyers. This direction thus represents only part of the solution and could lead to bidding wars between Europe and other LNG destinations (like India, Pakistan and Bangladesh). Besides, a prospect of one more “war” is looming on the horizon as the EU will have to mend ties with Algeria, which has reneged on the promise to expand the capacity of the Medgaz pipeline (from 8 to 10 bcm) after a row with Spain over Western Sahara.

Finally, the EU faces a lack of infrastructure to transport gas from its northwestern areas to Central and Eastern Europe as well as different infrastructures for L-gas and H-gas. In this respect, attention should be paid to the possibility of expanding the Trans-Adriatic Pipeline to 20 bcm by adding pump stations and the statements of Azerbaijan on producing more offshore gas. In another prominent move, Bulgaria and Greece have announced joint LNG purchases for Southeast Europe, clear seeking to enhance their future bargaining position inside the EU. Further to the south, EU diplomacy has already set its sights on developing energy cooperation with Israel, whose gas could be imported to Egypt via a pipeline and then shipped to Europe. But new deposits of gas there are yet to be discovered and developed to offset imports from Russia.

In conclusion, none of the aforementioned variables can be a quick panacea; rather, a cumulative effect of their combination, albeit still costly, will bear fruit in the long-term.

Китайський фактор також дасть про себе знати з точки зору зеленого переходу ЄС. На КНР припадає 67% світових поставок фотоелектричних модулів, необхідних для отримання відновлюваної енергії. Більше того, близько 80% компонентів для вітрових турбін та 97% кремнієвих пластин для сонячних панелей мають китайське походження, не кажучи вже про 45% світового полікремнію, що виробляється в Сіньцзяні, та 70% літій-іонних акумуляторів. Усвідомлюючи цю залежність, Урсула фон дер Ляєн під час свого нещодавнього візиту до Індії звернулася до Міжнародного сонячного альянсу , який зараз намагається позиціонувати себе як альтернативу Китаю та нарощувати виробництво відновлюваної енергії. Тим не менш, відносини між ЄС та КНР набагато менш схильні до перетворення на конфронтацію, подібну до російської. Пекіну потрібен європейський досвід для інтеграції планування енергетичної системи та розвитку ринку електроенергії, що підтверджено створенням Платформи енергетичного співробітництва ЄС-Китай (ECECP) у 2019 році. Намагаючись адаптуватися до нових обставин, Європейський Союз, ймовірно, розвиватиме це партнерство, що зароджується.

Also read:

Luftraum-Kontrolle: Europa, Russland und die Politik des Luftraumschutzes über der Ukraine

Von der Verteidigungszusammenarbeit zur europäischen Integration: Kann die Sicherheitsdynamik die Beziehungen zwischen der Türkei und der EU wiederbeleben?